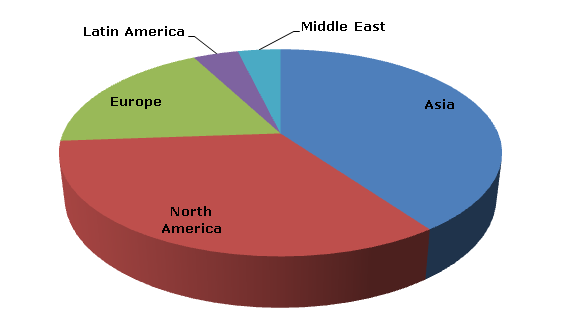

As of 2012, the world annual production capacity of ethylene-vinyl acetate (EVA) exceeded 5.87 million tonnes. In the same year Asia called for over 40% of the world’s total capacity. It was followed by North America and Europe, together holding a share of more than 52% of the total figure. Meantime, the USA, Taiwan, China, South Korea and Japan were the leading countries in terms of EVA capacity in 2012.

Ethylene-Vinyl Acetate (EVA): world capacity structure by region, 2012

Between 2009 and 2012, the global EVA production was following a stable upward trend, increasing by nearly 120,000 tonnes per year. In 2012, the world EVA production climbed to 3.54 million tonnes. In the same year, the EVA capacity utilization rate stood at around 60%.

As of 2012, the EVA production was concentrated in Asia and North America; the combined production of these two regions was estimated at more than 2.68 million tonnes. Top three EVA producing countries (namely, Taiwan, China and South Korea) stood at 954,000 tonnes.

Ethylene-Vinyl Acetate (EVA): major manufacturers worldwide, 2012

The dominant players operating in the worldwide EVA market include, among others, ExxonMobil, Lyondell Basell, DuPont Chemical, Versalis, SINOPEC, Formosa Plastics, Braskem, Hanwha Chemical, Westlake Chemical, Dow Chemical, Samsung Total PC and Arkema.

The countries of the APAC (except China and Japan), North America and Western Europe regions were the top exporters of EVA in 2012. Meantime, China together with the countries of the Middle East and Africa were the key importers of EVA.

The global EVA production is poised to witness steady growth in the upcoming years, driven by the increasing world demand coupled with scheduled capacity introductions. In 2017, the volume of the global EVA production is anticipated to surpass the 4.23 million tone mark.

More information on ethylene-vinyl acetate (EVA) market can be found in the research study “Ethylene-Vinyl Acetate (EVA): 2014 World Market Outlook and Forecast up to 2018”.