Arsenic and its compounds are firmly associated with toxicity and environmental risks. Detrimental impact of arsenic is a well-known fact. Its dangerous concentrations have been found in many parts of the world, while numerous remediation technologies and approaches combatting arsenic contamination have been proliferating. There is also no shortage of regulatory efforts to mitigate effects of such contamination. A voluntary agreement between the timber industry and the US government to move away from chromated copper arsenate (CCA) in wood treatment, (which is the main application segment for arsenic), is an inevitable response to the above concerns. With such a stigma, it is quite difficult to have long-lasting and strategic plans for the development of the arsenic market. Unsurprisingly, main arsenic trioxide manufacturing countries mostly belong to the developing world.

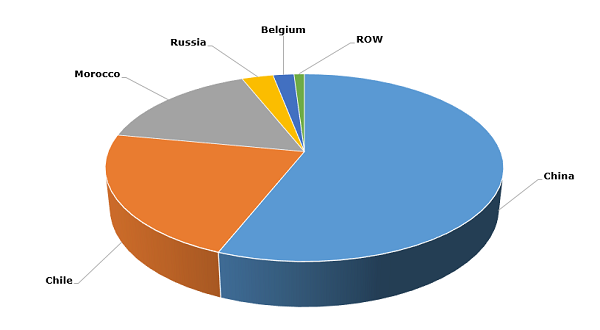

Arsenic trioxide: top manufacturing countries

For instance, arsenic trioxide and primary arsenic metal have not been produced in the United States since 1985. In the USA, limited quantities of arsenic metal have been recovered from gallium-arsenide (GaAs) semiconductor scrap, while most arsenic uses are limited to CCA application in the non-residential sector. The prospects of the global arsenic market are therefore not particularly bright due to high plausibility of other arsenic-related regulatory initiatives and easy availability of substitutes like monoethanolamine (MEA), demand for which immediately took off after the CCA ban. There is some potential for arsenic in certain specific industrial applications (marine timber treatment, GaAs components in cellular handsets and GaAs-based light-emitting diodes), but they are limited.

More details on the arsenic market can be found in the insightful research study “Arsenic: 2016 World Market Review and Forecast”.