Zirconium (Zr) is a grayish-white metallic element employed in ceramics, foundry, refractory, electronics, nuclear industry and other applications.

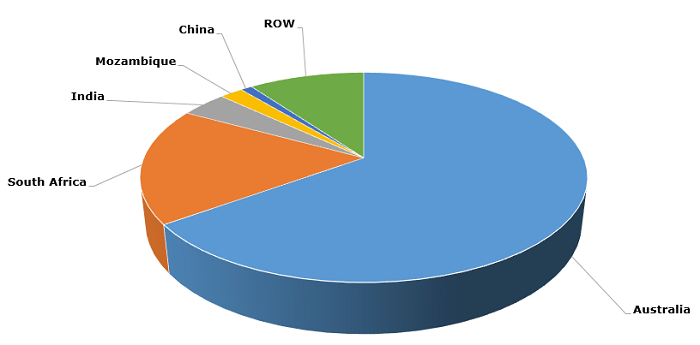

More than 80% of the world zirconium reserves are located in two countries: Australia (65%) and South Africa (18%). Zirconium production is concentrated in the hands of a few companies, including Iluka, Tronox and Richards Bay Mining.

Zirconium: structure of the world reserves by country, 2015

The market for zirconium concentrates is mainly driven by the demand from ceramics market; the ceramics sector is the largest end user of zircon, accounting for about 50% of demand. Approximately 90% of ceramics demand is related to tile manufacture, 9% to the production of other ceramics and 1% to tableware. The foundry, refractory, electronics and nuclear industries are the other major consumers. It is pertinent to mention that such industries as ceramics (and tile production) or refractory sector are highly susceptible to the state of the construction industry and as such to the general economic outlook, which is at best now looks like unstable.

Thus, the status of zircon-mining companies like Australia-based Iluka Resources or US-based Tronox, which are heavily involved in mineral sands operations, depends on the current market environment and demand-supply balance trajectories. Another important factor is their ability to diversify and spread all current risks among various products of their portfolio, as well as to flexibly adapt their utilization rates to all fluctuations on the market.

More information on the zirconium market can be found in the in-demand research study “Zirconium and Hafnium: 2017 World Market Review and Forecast”.