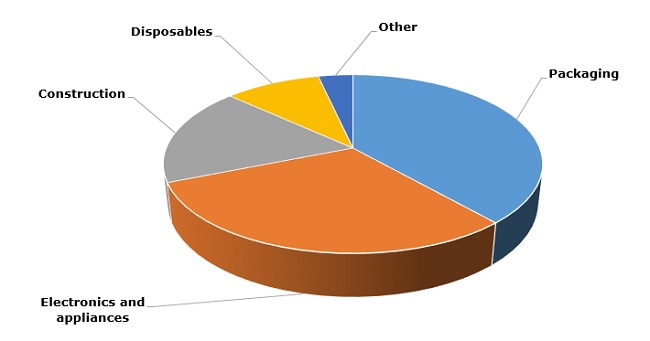

The global polystyrene market is characterised by high contingency and specificity subject to various dimensions and factors. Its complex dynamics depends on the interplay of different forces. These forces primarily include feedstock styrene monomer (SM) price fluctuations. Another important factor is behaviour of downstream sectors, like packaging, electronics, constructional insulation, etc.

Polystyrene: structure of the global market on the basis of applications

One should not underestimate the influence of seasonality. For instance, the month of February is a busy season for planned turnarounds at upstream styrene plants, which might spur polystyrene inventory building, though the end-of-year festivity season might intervene. One should not forget about environmental considerations (this factor heavily affects the polystyrene market) or antidumping duties (e.g. Japan’s actions against Chinese plastic imports). Such contingency and specificity make it difficult to describe the global polystyrene market in terms of some common characteristic trends. However, recent surges in oil prices and ensuing SM price rise are instrumental in affecting nearly all regional polystyrene markets. It is debatable whether this trend is long lasting since some experts predict it has a rather short-term outlook and the polystyrene market will soon arrive at some sort of equilibrium. They point to a synergy of several macroeconomic, seasonal and other factors behind oil price increases. Of course, styrene will become more expensive in the first quarter of 2018. However, these experts also draw comparisons with previous years, when such increases (they were even higher last year) were well handled by the polystyrene market.

More information on the polystyrene market can be found in the in-demand research report “Polystyrene (PS): 2018 World Market Outlook and Forecast up to 2027”.